July 14, 2026

Uninsured and Underinsured Motorist Coverage Explained

Hit by a driver with no insurance or too little? Uninsured motorist coverage protects you. Learn how UM and UIM work and why they matter in California.

Uninsured and Underinsured Motorist Coverage Explained

Quick answer: Uninsured and underinsured motorist coverage protects you when you're hit by a driver who has no insurance or not enough to cover your damages. Uninsured motorist coverage handles drivers with no insurance and hit-and-runs, while underinsured motorist coverage covers the gap when the at-fault driver's limits are too low. It mainly pays for your injuries and lost wages.

Table of contents

- What uninsured motorist coverage protects

- Uninsured vs underinsured: the difference

- What these coverages actually pay for

- Do you need uninsured motorist coverage?

- What California drivers should know

- How to add this coverage to your policy

- Frequently asked questions

Rosa was rear-ended at a light in Sacramento by a driver who, it turned out, had no insurance at all. She assumed his coverage would handle her medical bills, then learned he had none. That's exactly the gap uninsured motorist coverage is built to fill, and it's one of the most overlooked parts of an auto policy.

You can't control whether other drivers carry insurance, but you can protect yourself from the ones who don't. Here's what uninsured and underinsured motorist coverage actually does, what it pays for, and why skipping it can leave you paying for someone else's mistake out of pocket.

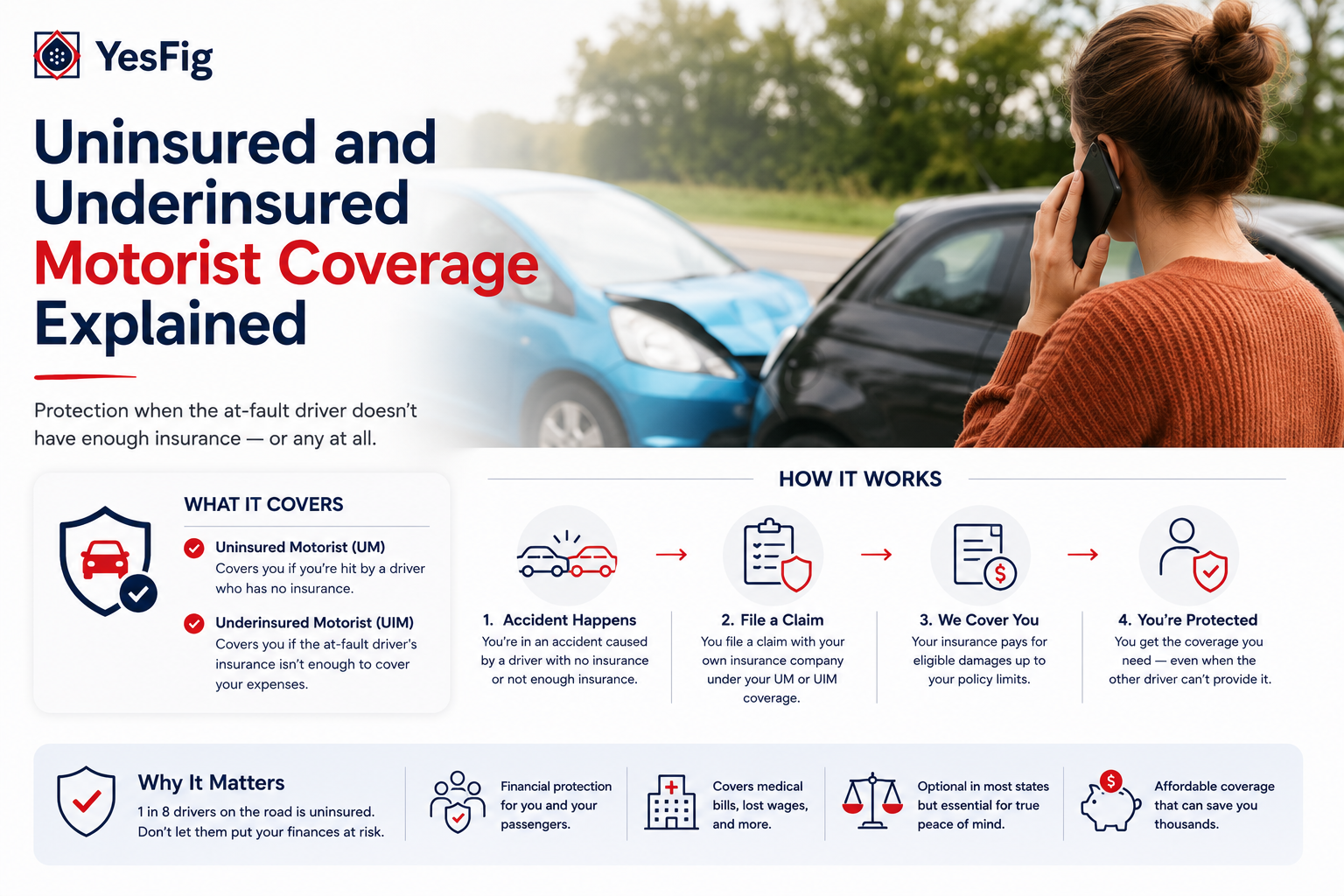

What uninsured motorist coverage protects

Uninsured motorist coverage steps in when you're in an accident caused by a driver who has no insurance. Instead of being stuck with your own bills, your policy covers you as if the at-fault driver had been insured. It also typically covers hit-and-run accidents, where the other driver flees and can't be identified.

This is different from your liability coverage, which pays for injuries and damage you cause to others. Uninsured motorist coverage protects you and your passengers. Get hit by an uninsured driver without it, and you could be stuck paying your own medical bills and lost wages, with little chance of recovering anything from someone who couldn't afford insurance in the first place.

Not sure if your policy has this coverage?

That's worth checking. Fig can explain how uninsured and underinsured motorist coverage works and show you what a California car insurance policy includes, with no pressure to switch.

Uninsured vs underinsured: the difference

The two coverages sound similar but handle different situations. Uninsured motorist coverage applies when the at-fault driver has no insurance at all, or in a hit-and-run. There's simply no policy on the other side to pay you.

Underinsured motorist coverage kicks in when the other driver does have insurance, but their limits are too low to cover your full damages. Say your injuries cost $60,000 and the at-fault driver only carries $30,000 in coverage. Their insurance pays its limit, and your underinsured motorist coverage can make up the difference, up to your own limit. One covers no insurance, the other covers not enough.

What these coverages actually pay for

Both come in two flavors. The main one is bodily injury coverage, which pays for your and your passengers' medical bills, lost wages, and pain and suffering when an uninsured or underinsured driver hurts you. This is the part most people count on.

There's also property damage coverage in some states, which pays to repair your vehicle after an uninsured driver hits it, though it can overlap with collision coverage. Adding these protections to California car insurance fills the exact gap that other drivers' missing or minimal coverage leaves behind.

Good to know: Uninsured motorist coverage typically covers hit-and-run accidents, where the at-fault driver flees and can't be identified. Since there's no one to collect from, your own coverage steps in to pay for your injuries, which is protection you can't get any other way.

Want to know if you're covered against uninsured drivers?

A quick review answers it. Yesfig can check whether your policy includes uninsured and underinsured motorist coverage and show you the cost to add it. Compare your car insurance in a few minutes.

Do you need uninsured motorist coverage?

For most drivers, it's some of the most valuable coverage you can carry. A meaningful share of drivers on the road are uninsured or carry only minimum limits, and you have no say in who hits you. If one of them causes a serious accident, this coverage is often the only thing standing between you and a stack of your own bills.

It matters even more when other drivers carry only the legal minimum. If someone with bare-minimum liability injures you badly, their limits can run out fast, and your underinsured motorist coverage is what fills the rest. For Rosa, having it would have turned a stressful, expensive ordeal into a covered claim.

What California drivers should know

California has a couple of specifics worth knowing. Insurers here must offer uninsured and underinsured motorist coverage, but it isn't mandatory, so you can decline it in writing. Many drivers do, often without realizing what they're giving up.

Two facts make it worth keeping in California. The state has a notable share of uninsured drivers, and its minimum liability limits mean plenty of insured drivers carry only modest coverage. Both raise the odds that an at-fault driver can't fully cover your damages. Yesfig Insurance, a Los Angeles-based brand of Focus Insurance Group, offers auto coverage across California and can include this protection on your policy.

Key takeaways

- Uninsured motorist coverage protects you when an at-fault driver has no insurance or flees.

- Underinsured motorist coverage covers the gap when their limits are too low.

- It mainly pays your medical bills, lost wages, and pain and suffering, unlike liability.

- In California, insurers must offer it, but you can decline, so confirm you have it.

How to add this coverage to your policy

Adding it is simple, and usually affordable. Here's the approach in three steps:

- Check your current policy. Confirm whether you already carry uninsured and underinsured motorist coverage, since many people don't.

- Match your limits. A common approach is to set these limits to match your liability coverage, so you're protected at the same level.

- Add it and keep it. If you can, include both the bodily injury and property damage portions, and don't decline it to save a little.

Do that and you're covered no matter how insured the other driver turns out to be. For more on building your coverage, the Yesfig blog breaks it down without the jargon.

Frequently asked questions

What is uninsured motorist coverage?

It's coverage that protects you when you're in an accident caused by a driver who has no insurance, or in a hit-and-run where the driver can't be identified. Your own policy pays for your injuries and losses as if the at-fault driver had been insured. It covers you and your passengers, not other people.

What's the difference between uninsured and underinsured motorist coverage?

Uninsured motorist coverage applies when the at-fault driver has no insurance at all, or flees in a hit-and-run. Underinsured motorist coverage applies when the driver has insurance, but their limits are too low to cover your full damages. Your underinsured coverage then makes up the difference, up to your own limit.

Does uninsured motorist coverage cover hit-and-run accidents?

Usually, yes. When an at-fault driver flees and can't be identified, there's no insurance to collect from, so your uninsured motorist coverage steps in to pay for your injuries. This makes it valuable protection you can't get any other way, since you can't recover from a driver you can't find.

Do I need uninsured motorist coverage?

For most drivers, it's highly worthwhile. A meaningful share of drivers are uninsured or carry only minimum limits, and you can't control who hits you. Without this coverage, a serious accident caused by such a driver could leave you paying your own medical bills and lost wages, with little chance of recovering the money.

Is uninsured motorist coverage required in California?

No. California requires insurers to offer uninsured and underinsured motorist coverage, but you can decline it in writing, so it isn't mandatory. Given the state's share of uninsured drivers and its minimum liability limits, though, keeping this coverage is usually a smart move rather than something to reject to save a little.

You can't make other drivers carry insurance, but you can make sure their gaps don't become yours. If Rosa had carried uninsured motorist coverage, her rear-end accident would have been a straightforward claim instead of a financial headache. Add this protection to your policy, and a careless, uninsured driver stays their problem, not yours.

Ready to protect yourself from uninsured drivers?

Get a car insurance quote in minutes with Yesfig. Coverage in California starts at $30/mo, and a licensed advisor can add uninsured and underinsured motorist protection sized to your policy. Covered no matter who hits you.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.