June 4, 2026

Term Life vs Universal Life Insurance Explained

Term life vs universal life insurance, explained for Californians: how they differ on cost, cash value, and duration, plus how to pick the right one.

Term Life vs Universal Life Insurance: How to Tell Them Apart

Quick answer: Term life insurance covers you for a set period, usually 10 to 30 years, and is the cheapest way to protect your family, with no cash value. Universal life is permanent, costs more, and builds cash value you can borrow against. For most Californians protecting an income or a mortgage, term life is the practical choice.

Table of contents

- What is term life insurance?

- What is universal life insurance?

- Term life vs universal life: the key differences

- How much each costs in California

- Term life vs universal life: which is right for you?

- Frequently asked questions

Marcus just had his first kid in San Diego, and now there are two life insurance quotes open in his browser tabs. One is cheap and simple. The other costs a lot more and comes with a page of words like "cash value" and "flexible premiums." He's not sure which one a responsible new dad is supposed to pick. If you're stuck in the same spot, the term life vs universal life insurance decision is mostly about one question: do you need coverage for a chunk of your life, or for all of it?

Here's the plain-English version, with California specifics, so you can decide without the jargon fog.

What is term life insurance?

Term life insurance is coverage for a fixed period, called the term. You pick a length, commonly 10, 20, or 30 years, and pay a level premium the whole time. If you die during the term, your beneficiaries get the death benefit, tax-free in almost every case. If you outlive the term, the policy simply ends.

That's the whole product. No investment account, no cash value, no moving parts. Because it only has to cover a set window, term is the cheapest way to buy a large death benefit, which is why it's the go-to for parents and homeowners protecting an income or a mortgage. Yesfig Insurance, a brand of Focus Insurance Group based in Los Angeles, offers California term life coverage starting at around $9 a month, with real numbers depending on your age, health, and coverage amount.

Still sorting out the basics?

That's exactly what Fig is for. Get plain-English answers about how much coverage you actually need before you commit to a policy type, and browse the Yesfig insurance blog for more buyer guides.

What is universal life insurance?

Universal life insurance (UL) is a type of permanent life insurance. As long as it stays funded, it covers you for your entire life, not just a term. Part of your premium pays for the insurance, and part goes into a cash value account that grows over time, usually based on an interest rate set by the insurer.

The headline feature is flexibility. Within limits, you can adjust your premium payments and even your death benefit as your life changes. You can also borrow against the cash value later. The tradeoff: UL is more expensive and more complex, and if the cash value runs too low to cover costs, the policy can lapse. There are several flavors, including guaranteed, indexed, and variable universal life, each with different risk and return profiles.

Good to know: California gives you a free-look period to cancel a brand-new life policy for a full refund, commonly 10 days and longer for some buyers, such as applicants age 60 and older. The California Department of Insurance sets these consumer protections, so you're never locked in the moment you sign.

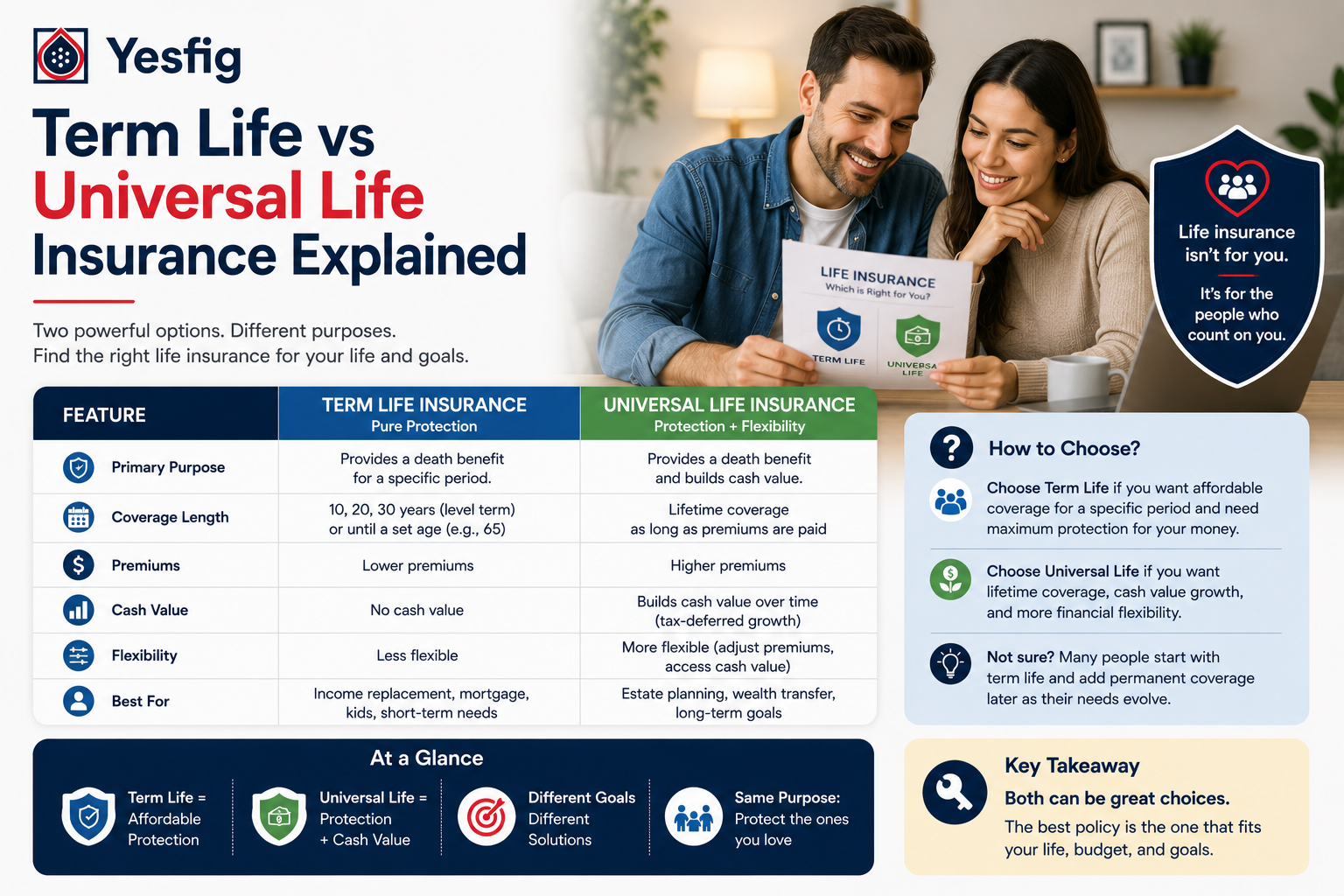

Term life vs universal life: the key differences

Strip away the sales language and the two products differ on a handful of things that actually matter:

| Feature | Term life | Universal life |

|---|---|---|

| Coverage length | Set term (10 to 30 years) | Permanent (lifelong, if funded) |

| Cost for the same death benefit | Lowest | Several times higher |

| Cash value | None | Builds over time |

| Premiums | Fixed and level | Adjustable within limits |

| Death benefit | Fixed | Often adjustable |

| Complexity | Simple | More moving parts; can lapse if underfunded |

| Best fit | Income or mortgage protection on a budget | Lifelong needs, estate planning, cash-value goals |

The short read: term trades permanence for a much lower price and total simplicity. Universal life trades affordability for lifelong coverage plus a savings component you can use down the road. Neither is "better." They solve different problems.

Key takeaways

- Term life is temporary, cheap, and simple. Universal life is permanent, pricier, and built around cash value.

- For the same death benefit, a permanent policy commonly costs several times more than term.

- Most people protecting a temporary need (kids at home, a mortgage) get more protection per dollar from term.

How much each costs in California

Cost is usually where the term life vs universal life insurance decision gets settled. For the same coverage amount, term wins on price, often by a wide margin. A healthy person can lock in a sizable term policy for a modest monthly premium, while a comparable universal life policy commonly costs several times more because you're funding both the insurance and the cash value.

Your real California rate depends on a few honest variables:

- Your age and health at the time you apply. Younger and healthier means cheaper, which is why locking in early pays off.

- The death benefit you choose. A common rule of thumb is 10 to 12 times your annual income, but match it to your actual obligations.

- The term length (for term) or the funding level (for universal life).

Fig tip: Don't buy more permanence than your situation needs. If your goal is "make sure the kids and the mortgage are covered until they're grown," a 20- or 30-year term usually does that job for a fraction of a permanent policy's cost. Fig can run the numbers both ways in real time.

Want to see how the two stack up for your budget?

Yesfig maps your coverage needs against your budget and shows you where term fits, no pressure. Compare California term life options in a few minutes and see a real starting number instead of a guess.

Term life vs universal life: which is right for you?

Start with how long you need the coverage, because that single answer points you to the right product.

Term life is usually the better fit if you:

- Want to protect a temporary need, like income while your kids are home or the years left on a mortgage.

- Need the largest death benefit your budget allows.

- Prefer a simple policy you can set and forget.

Universal life can make sense if you:

- Want coverage that lasts your whole life, not just a term.

- Have a lifelong dependent or specific estate-planning goal.

- Genuinely want a cash-value component and understand the fees and lapse risk that come with it.

A quick gut check: most young families and new homeowners in California are protecting a temporary stretch of life, so term gives them more protection per dollar. If you're also worried about a sudden accident specifically, you can pair coverage with a California accidental death policy for added protection. Worth knowing up front: Yesfig focuses on term life in California and doesn't sell universal life, so if a permanent policy is truly what you need, an honest advisor will tell you that too.

Frequently asked questions

Is term life or universal life cheaper?

Term life is cheaper, usually by a wide margin, for the same death benefit. Universal life costs more because your premium funds both the insurance and a growing cash value account. If price is your main concern and your need is temporary, term gives you the most coverage per dollar.

Does term life insurance build cash value?

No. Term life has no cash value or investment component, which is exactly why it costs less. It pays a death benefit if you pass away during the term, and nothing if you outlive it. Universal life and other permanent policies are the ones that build cash value over time.

What happens when my term life policy ends?

When the term ends, coverage stops. You typically can renew at a much higher age-based rate, convert to a permanent policy if your contract allows, or simply let it lapse if you no longer need it. Many people plan the term length to match how long the need lasts.

Can I switch from term to permanent life later?

Often, yes. Many term policies include a conversion option that lets you switch to a permanent policy without a new medical exam, within a set window. Read your policy terms, since the conversion deadline and available permanent products vary by insurer. Ask before you assume it's included.

Which type of life insurance do most California families choose?

Most California families protecting an income or a mortgage choose term life, because it delivers a large death benefit at the lowest cost. Universal life appeals to a smaller group with lifelong coverage needs or specific cash-value and estate-planning goals who can afford the higher premiums.

The bottom line

Marcus closed one of those browser tabs. With a young kid and a 30-year mortgage ahead of him, a term policy covered the years that actually needed covering, for a price that didn't make him wince. That's the usual answer for a temporary need: term life does the heavy lifting affordably, and universal life is the right call only when lifelong coverage and cash value are genuinely your goal. Pick based on how long you need protection, not on which one sounds fancier.

Ready to protect your people?

Get a California term life quote with Yesfig in minutes. Coverage starts at around $9 a month, and a licensed advisor is there if you want a human to walk you through it.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.