May 23, 2026

Term Life vs. Universal Life Insurance Compared

Term vs. universal life insurance: term is cheaper and simpler, universal lasts for life and builds cash value. Here's how to pick the right one.

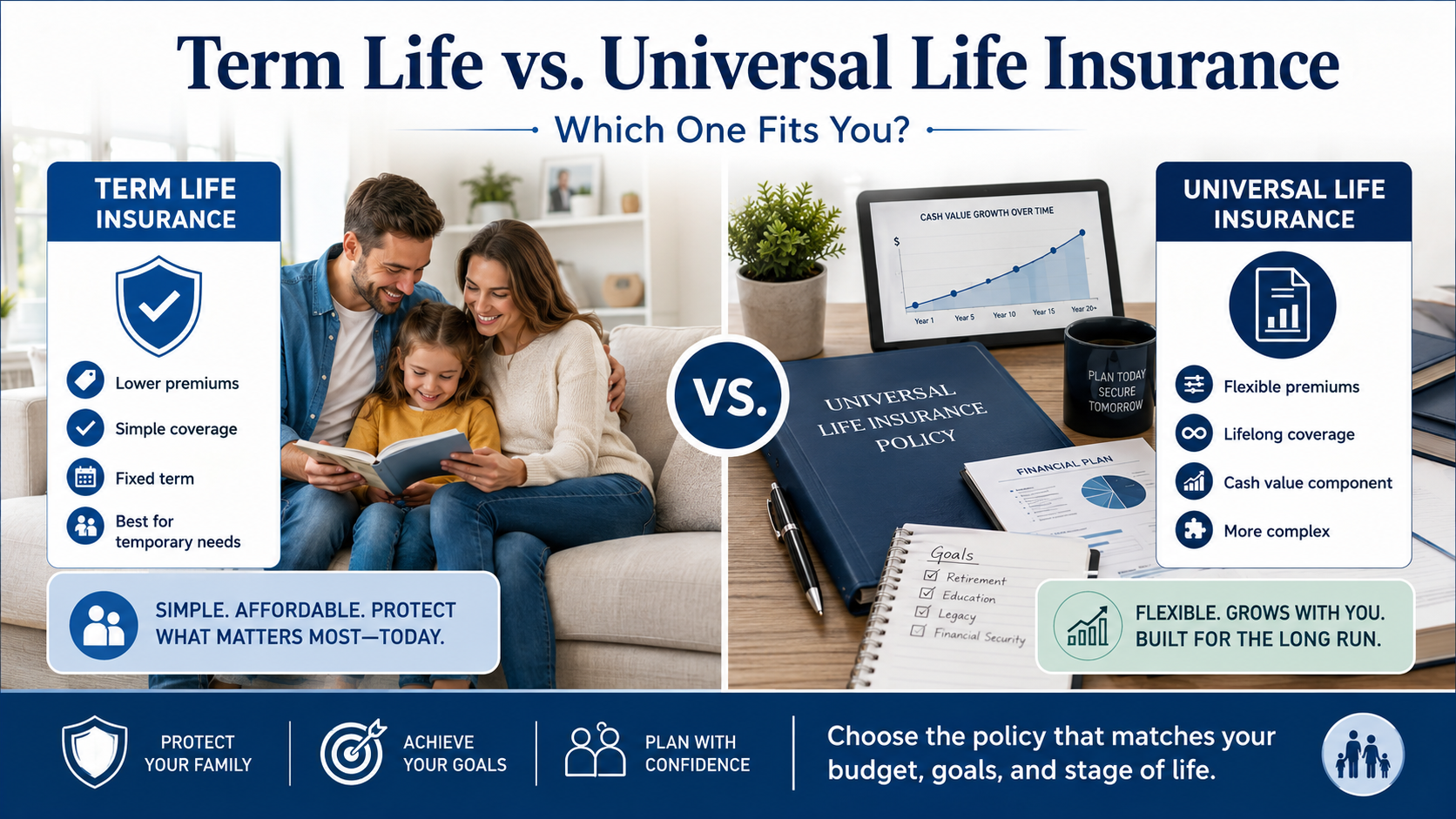

Term Life vs. Universal Life Insurance: Which One Fits You?

Quick answer: Term life insurance is cheaper and covers a set period (10 to 30 years), making it the right fit for most people who need protection during their working years. Universal life costs more but lasts your whole life and builds cash value you can borrow against. Choose term for affordable, temporary protection; choose universal for lifelong coverage and a flexible savings component.

Table of contents

- The two policies at a glance

- How term life works

- How universal life works

- Side-by-side comparison

- Which one fits your situation

- How to decide and get covered

- Frequently asked questions

When Maria sat down to sort out life insurance, she hit the same wall most people do. Two main options kept coming up, term life and universal life, and the explanations online seemed designed to confuse her. A 38-year-old marketing manager in San Diego with two kids and a mortgage, she just wanted to know which one made sense for her, not a lecture on insurance theory.

So she did what you're probably doing right now: she lined them up side by side. Here's the comparison the way Maria worked through it, so you can land on your own answer by the end.

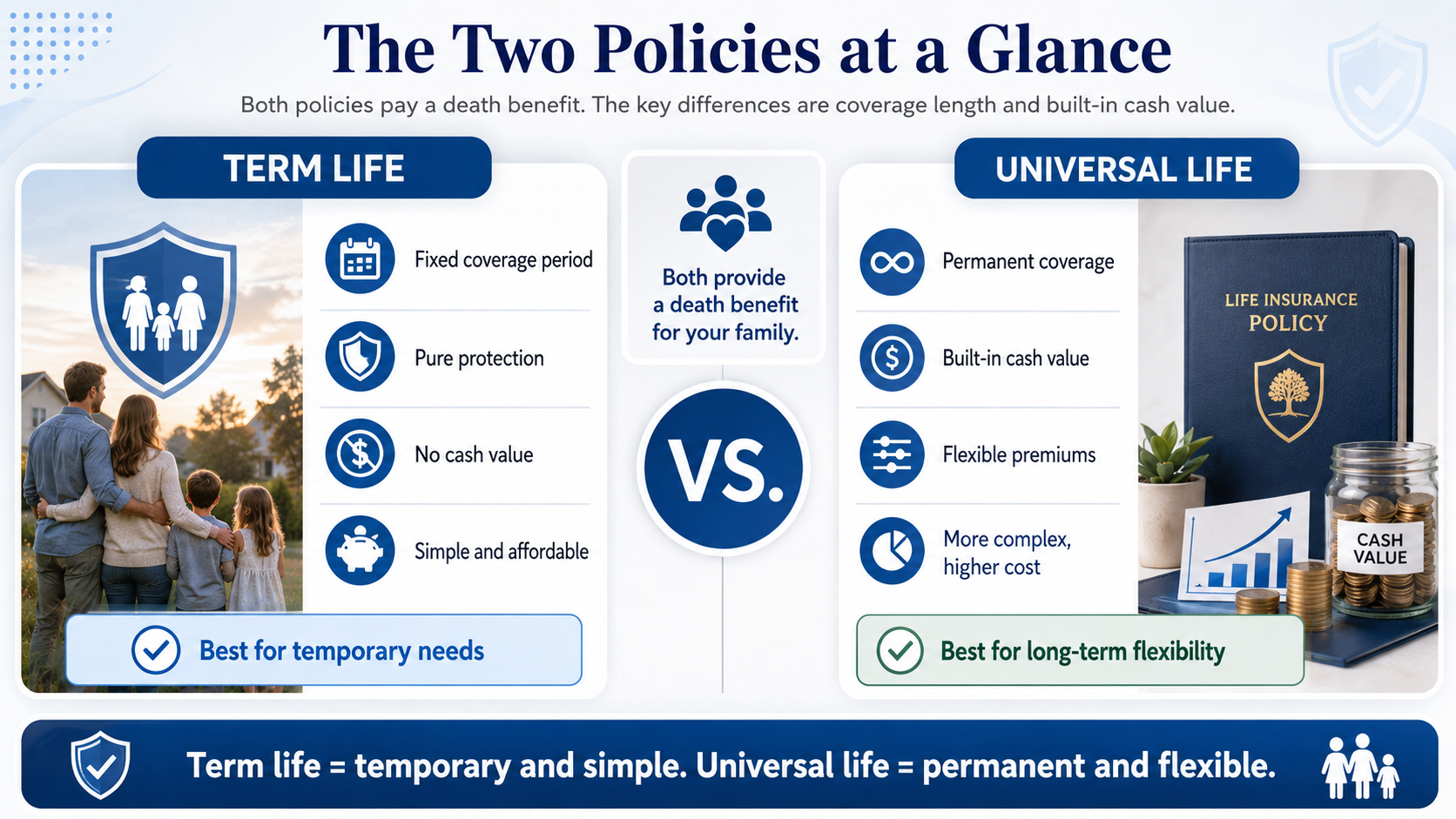

The two policies at a glance

Both term and universal life pay your family a death benefit if you pass away. The difference is how long the coverage lasts and whether it builds value while you hold it.

Term life is pure protection for a fixed window. Universal life is permanent coverage with a built-in cash value account and flexible premiums. That single distinction, temporary-and-simple versus permanent-and-flexible, drives almost every other difference in price, complexity, and who each one suits.

Not sure which camp you're in?

That's what Fig is for. See how life insurance options compare and get plain answers before you commit to anything.

How term life works

Term life insurance covers you for a set period, usually 10, 20, or 30 years, at a level premium. If you die during the term, your family gets the death benefit. If the term ends and you're still here, the coverage simply expires.

This is what drew Maria in first. Her real worry was the next 20 years, until the mortgage is paid and her kids are through college. Term life covers exactly that window for a low, predictable monthly cost, often around $9 to $40 a month for a healthy adult her age. No cash value, no moving parts, just protection for the years it matters most.

How universal life works

Universal life insurance is permanent coverage that never expires as long as you fund it, and it includes a cash value account that grows over time. You can adjust your premiums and death benefit within limits, and you can borrow against the cash value later.

Maria found the lifelong angle appealing, until she saw the price. Universal life can cost several times more per month than term for the same death benefit, because part of your premium funds the cash value and part covers the cost of lifelong insurance. It's a real tool for specific goals, like leaving an inheritance no matter when you pass, or estate planning. But it asks more of your budget and more of your attention.

Good to know: Universal life's cash value and flexible premiums make it more complex to manage than term. If a policy isn't funded enough over time, the rising cost of insurance can eat into the cash value. It's worth reviewing with a licensed advisor rather than setting and forgetting.

Side-by-side comparison

Here's the lineup Maria built:

| Feature | Term life | Universal life |

|---|---|---|

| Coverage length | Fixed term (10 to 30 years) | Lifelong |

| Monthly cost | Low | Several times higher |

| Cash value | None | Yes, grows over time |

| Premium flexibility | Fixed and level | Adjustable within limits |

| Complexity | Simple | Requires active management |

| Best for | Income protection during working years | Lifelong coverage, estate planning |

Key takeaways

- Term life is cheaper, simpler, and covers a set period.

- Universal life costs more, lasts for life, and builds cash value.

- Most people protecting their family during working years are best served by term.

Want to see real numbers for both?

You don't have to guess at the price gap. Yesfig and Fig can quote term and walk you through whether permanent coverage is worth it for your goals. Compare your life insurance options in a few minutes.

Which one fits your situation

For Maria, the choice got clear once she named what she actually needed. Her goal was protecting her family's income for a defined stretch of years, not building a lifelong financial instrument. That's the textbook case for term, and it's where most young families, new parents, and homeowners with a mortgage land.

Universal life makes more sense if you want coverage that's guaranteed to pay out whenever you pass, you've already maxed other tax-advantaged savings, or you have estate-planning needs like leaving a set inheritance. If that's you, the higher cost buys something term can't: permanence. The honest answer for most people, though, is that term covers the real need for a fraction of the cost, and the money saved can do more in a straightforward retirement account.

How to decide and get covered

Maria settled it in three steps, and you can too:

- Name your goal. Temporary protection for your working years points to term. Lifelong coverage or estate planning points to universal.

- Compare real quotes with Fig. See term priced against your coverage target, and weigh whether permanent coverage earns its higher cost for you.

- Lock it in. A licensed advisor can confirm your choice, and your term rate stays level for the full period.

Frequently asked questions

Is term or universal life insurance better?

Neither is universally better; they suit different goals. Term life is better for most people who need affordable protection during their working years, like new parents or homeowners with a mortgage. Universal life is better for those who want lifelong coverage and a cash value component, often for estate planning, and who can afford the substantially higher premiums.

Why is universal life so much more expensive than term?

Universal life costs more because it provides lifelong coverage and builds cash value, while term only covers a fixed period with no savings element. Part of every universal life premium funds the cash value account and the cost of insuring you for life, so the same death benefit costs several times more per month than an equivalent term policy.

Can you convert term life to permanent coverage later?

Many term policies include a conversion option that lets you switch to permanent coverage without a new medical exam, usually within a set window. This can be useful if your needs change. The exact terms vary by policy, so it's worth confirming the conversion details with a licensed advisor before you buy.

Which is better for a young family in California?

For most young California families, term life is the better fit. It delivers the largest death benefit for the lowest monthly cost, covering the years when children are dependent and a mortgage is being paid. Universal life can be added later for specific lifelong or estate-planning goals if the budget allows.

The clearer your goal, the easier the choice

By the time Maria finished her side-by-side, the decision had basically made itself. She didn't need a perfect grasp of every insurance term, she just needed to know what she was protecting and for how long. Once that was clear, term was the obvious fit, and she had it in place by the weekend. Picture that same clarity for yourself: not two confusing products, just one good answer and the calm that comes after it.

Ready to find your fit?

Get a life insurance quote in minutes with Yesfig. Compare term against permanent coverage with Fig, and a licensed advisor is there if you want a human in the loop.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.