June 15, 2026

The Real Cost of Term Life Insurance at Every Age

What does term life insurance cost at every age? See how premiums rise as you get older, what drives the price, and why buying early locks in lower rates.

The Real Cost of Term Life Insurance at Every Age

Quick answer: Term life insurance cost rises with age, because the price reflects risk and risk grows over time. A healthy person in their 20s or 30s pays the least, with premiums climbing gradually through the 40s and more steeply in the 50s and 60s. Buying earlier and locking in a level-term rate keeps the cost low.

Table of contents

- What drives term life insurance cost

- Term life insurance cost in your 20s and 30s

- Term life insurance cost in your 40s and 50s

- Term life insurance cost in your 60s and beyond

- Why age matters so much

- How to keep your term life insurance cost low

- Frequently asked questions

At 34, Marcus keeps telling himself he'll sort out life insurance next year. He's healthy, busy, and figures the price will be about the same whenever he gets around to it. That last part is the expensive mistake. Term life insurance cost is tied tightly to your age, and it climbs every year you wait. Understanding how the price moves over a lifetime is the difference between locking in a low rate and paying more for the same coverage later.

The pattern is consistent and worth knowing, because it turns a vague "someday" into a clear reason to act. Here's how the cost actually behaves across the decades.

What drives term life insurance cost

Price comes down to risk, and several factors shape it. The biggest by far is age, since the chance of a claim rises as you get older. But it's not the only lever.

- Health. Conditions, weight, and family history all factor in, and a medical exam often sets your rate.

- Coverage amount and term length. More coverage and a longer term mean a higher premium.

- Smoking and lifestyle. Tobacco use can multiply your rate, and risky hobbies can raise it.

- Sex. Because life expectancy differs on average, women often pay slightly less for the same coverage.

Age sits at the center because it's the one factor guaranteed to move against you over time. That's what makes the timing of your purchase matter so much, and why getting a real quote on a California term life policy reflects your own mix of these factors.

Wondering what you'd actually pay right now?

Your real number depends on your age, health, and coverage amount, and it's quick to find out. Fig can explain what drives your rate, in plain English, before you commit. Start with the basics of term life insurance in California.

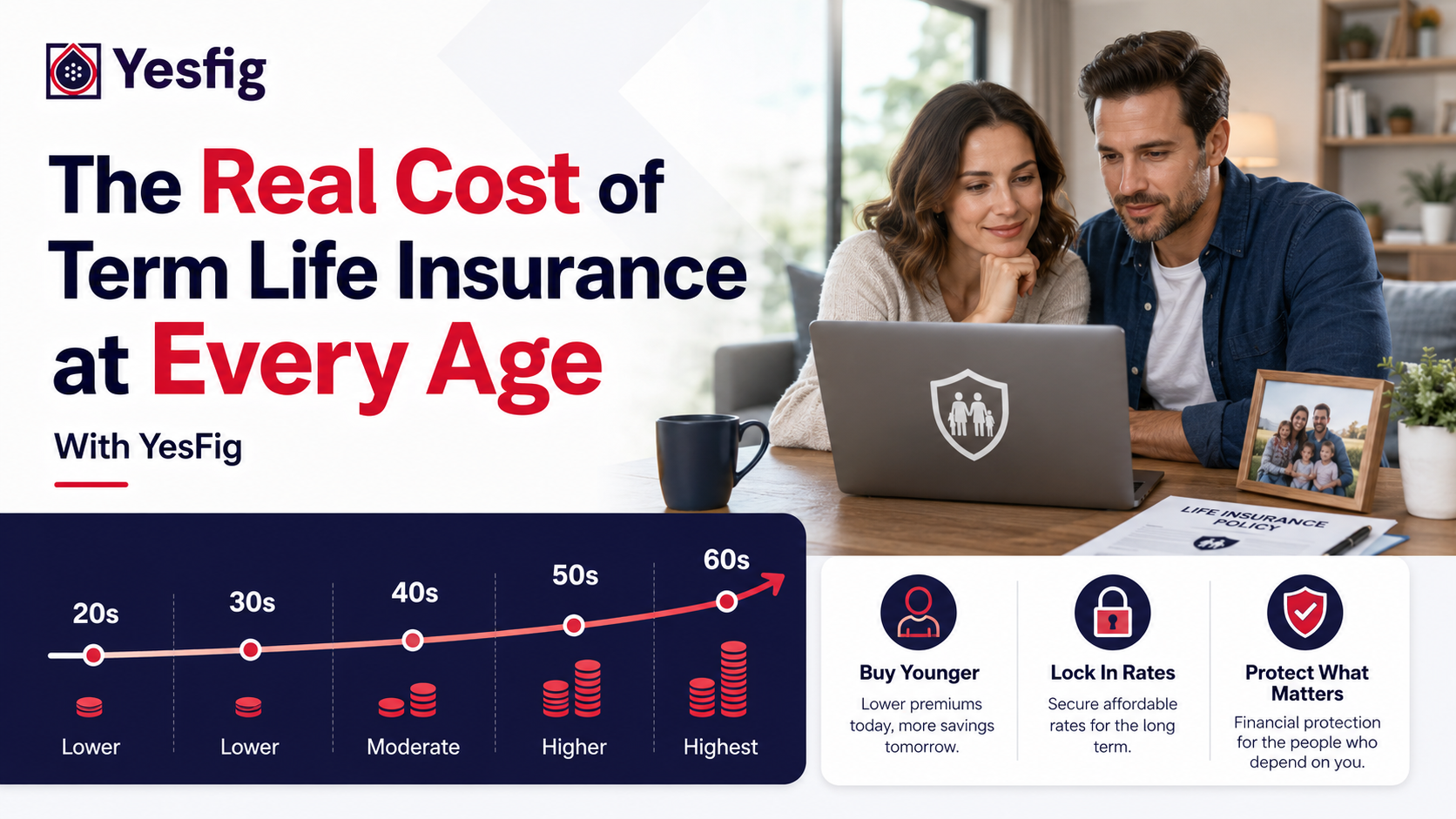

Term life insurance cost in your 20s and 30s

This is the cheapest coverage will ever be, full stop. In your 20s and 30s, you're statistically low risk, usually in good health, and insurers price that accordingly. It's common for young, healthy California residents to find term coverage starting at just a few dollars a month.

The catch is that this is also when people feel least urgency, since the need can seem far off. But buying now does two things at once: it locks in a low rate for your whole term, and it secures coverage before any health changes can raise the price or complicate approval.

If you have a partner, kids, a mortgage, or shared debt, the case is even stronger. Locking in young is the closest thing to a discount the system offers.

Term life insurance cost in your 40s and 50s

By your 40s, premiums have begun their climb, though coverage is still very affordable for most healthy people. This is often when life insurance feels most relevant, with dependents and a mortgage in full swing, so demand and need line up.

The shift gets sharper in your 50s. Risk rises more noticeably, minor health issues become more common, and both factors push the price up faster than in earlier decades. Coverage is still well worth having here, but the same policy now costs meaningfully more than it would have a decade earlier. Some buyers in this stage also pair a policy with an accidental death policy for added protection during peak family years.

The takeaway for this stage: it's still a smart buy, just a pricier one than waiting made it.

Term life insurance cost in your 60s and beyond

In your 60s and later, term life insurance cost rises steeply. Risk climbs, the medical underwriting matters more, and available term lengths often shorten because insurers are pricing a higher-probability window.

Coverage is still obtainable and can absolutely make sense, especially to cover remaining debt, final expenses, or a dependent. But this is where the cost of having waited shows up most plainly. The premium for a policy bought at 65 reflects a very different risk picture than the same coverage bought at 35.

Key takeaways

- Age is the single biggest factor in term life pricing.

- A level-term policy locks your rate for the whole term once you buy.

- Premiums to buy new coverage rise gradually early, then steeply later in life.

- Buying young and healthy is the most reliable way to pay less.

Why age matters so much

Here's the nuance that changes how you should think about timing. With a level term policy, your premium is fixed for the entire term you choose, whether that's 10, 20, or 30 years. It does not rise each year as you age. You lock today's rate and keep it.

Good to know: With level term life insurance, your premium is locked in for the entire term, so it doesn't rise year to year once you buy. What gets more expensive is purchasing a new policy as you age. Term life through Yesfig is available to California residents and can start around $9/mo. Yesfig Insurance is a brand of Focus Insurance Group based in Los Angeles.

So when people say term life "gets more expensive every year," what they really mean is that buying a new policy gets more expensive every year. Waiting doesn't keep your options frozen at today's price; it resets them at tomorrow's age. That's the real cost of delay.

How to keep your term life insurance cost low

You can't stop aging, but you control most of the other levers. To pay as little as possible:

- Buy younger. Age is the biggest factor and it only moves one way, so sooner almost always beats later.

- Lock in while you're healthy. Securing coverage before health changes protects both your rate and your eligibility.

- Right-size the policy. Match the term length and coverage amount to your actual need rather than overbuying.

- Compare before you assume. Rates vary, so a quick quote beats guessing at the price.

Do those four and you've squeezed most of the savings available. Your exact premium still depends on your personal details, so a quote is the only way to see your real number. A licensed Yesfig advisor can help you weigh term length against coverage amount.

Trying to decide between buying now or later?

The math almost always favors sooner, but it's worth seeing for yourself. Yesfig can show how term length and coverage amount shape your rate at your current age. Explore term life options and compare.

Frequently asked questions

How much does term life insurance cost?

It varies based on your age, health, coverage amount, and term length, so there's no single price. Young, healthy California residents can find term coverage starting at just a few dollars a month, with costs rising as you get older. Because the factors are personal, a quick quote is the only way to see your real number.

Why does term life insurance get more expensive with age?

Because the price reflects risk, and the likelihood of a claim rises as you age. Insurers price that increasing risk into each new policy. The jump is gradual in your 30s and 40s, then steeper in your 50s and 60s, which is why locking in coverage earlier almost always costs less over the long run.

Does my premium go up every year with term life?

Not with level term life. Once you buy a level-term policy, your premium is fixed for the entire term you chose, whether 10, 20, or 30 years. It won't rise as you age during that window. What increases each year is the cost of buying a brand-new policy later, which is the real penalty for waiting.

Is it cheaper to buy term life insurance when you're young?

Yes, significantly. Your 20s and 30s are when coverage is cheapest, because you're statistically low risk and usually in good health. Buying then locks in a low rate for your full term and secures coverage before any health changes can raise the price or complicate approval. It's the most reliable way to pay less.

What factors affect term life insurance cost besides age?

Several. Your health, including conditions, weight, and family history, plays a major role and is often checked with a medical exam. The coverage amount and term length you choose affect the price, as does tobacco use, which can substantially raise rates. On average, women pay slightly less than men for the same coverage.

The cheapest day to buy is today

Term life insurance cost is a moving target, and it only moves upward with age. The good news is that buying a level-term policy freezes your rate for the whole term, so the youngest, healthiest version of you sets the price you keep. Like Marcus is learning, "next year" isn't a neutral choice. It's a more expensive one.

Ready to lock in today's age?

Get a California term life quote with Yesfig in minutes. Coverage starts around $9/mo, and buying now locks in a rate based on the youngest you'll ever be again.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.