June 2, 2026

How to Switch Homeowners Insurance Without a Coverage Gap

Learn how to switch homeowners insurance without a coverage gap. A step-by-step timing guide for California homeowners, plus how to avoid a costly lapse.

How to Switch Homeowners Insurance Without a Coverage Gap

Quick answer: To switch homeowners insurance without a coverage gap, set your new policy to start the same day your old one ends, then cancel the old policy only after the new one is active. A one-day overlap is fine. A lapse, even for a single day, is the real risk.

Table of contents

- What is a homeowners insurance coverage gap?

- Why switching carriers can accidentally create a gap

- How to switch homeowners insurance without a gap

- Time the switch around your renewal and your mortgage

- Mistakes that quietly leave you exposed

- Frequently asked questions

- Switch with confidence, not crossed fingers

Daniel opened his renewal notice in Sacramento and saw the thing a lot of California homeowners have seen lately: the premium jumped again. He wants a better rate, but one worry keeps stalling him. What if there's a day where neither policy is active, and that's the day a pipe bursts? That worry has a name. It's the coverage gap, the quiet stretch between two policies where you're left uninsured.

Here's the good news. Switching homeowners insurance is usually simple, and you can absolutely do it without a gap. You just have to get the timing right. Below is exactly how the pieces line up.

What is a homeowners insurance coverage gap?

A coverage gap is any stretch of time when your home has no active policy, even a single day. During that window, anything that happens (a fire, a break-in, someone hurt on your property) is yours to pay for, out of pocket.

There's a second sting if you have a mortgage. Your mortgage lender requires continuous coverage as a condition of the loan. If your policy lapses, the lender can buy a force-placed policy for you, and that coverage is usually far pricier and protects the lender, not your belongings. A solid California homeowners insurance policy is what stands between you and that bill, so the goal when switching is to keep one active at all times.

Why switching carriers can accidentally create a gap

Most gaps aren't reckless, they're just bad timing. The classic mistake is canceling the old policy first to stop paying for it, then letting the new one start a few days later. Those few days are uninsured.

Two other quiet causes show up a lot. One is setting the new policy's effective date for after the old one expires, instead of the same day. The other is an escrow mix-up, where the lender keeps paying the old carrier or fails to fund the new one on time. The fix for all three is the same: control the dates yourself, and don't cancel anything early.

Still figuring out what your home actually needs?

That's what Fig is for. You can look at your California homeowners options and get plain-English answers about coverage levels and deductibles before you change a single thing.

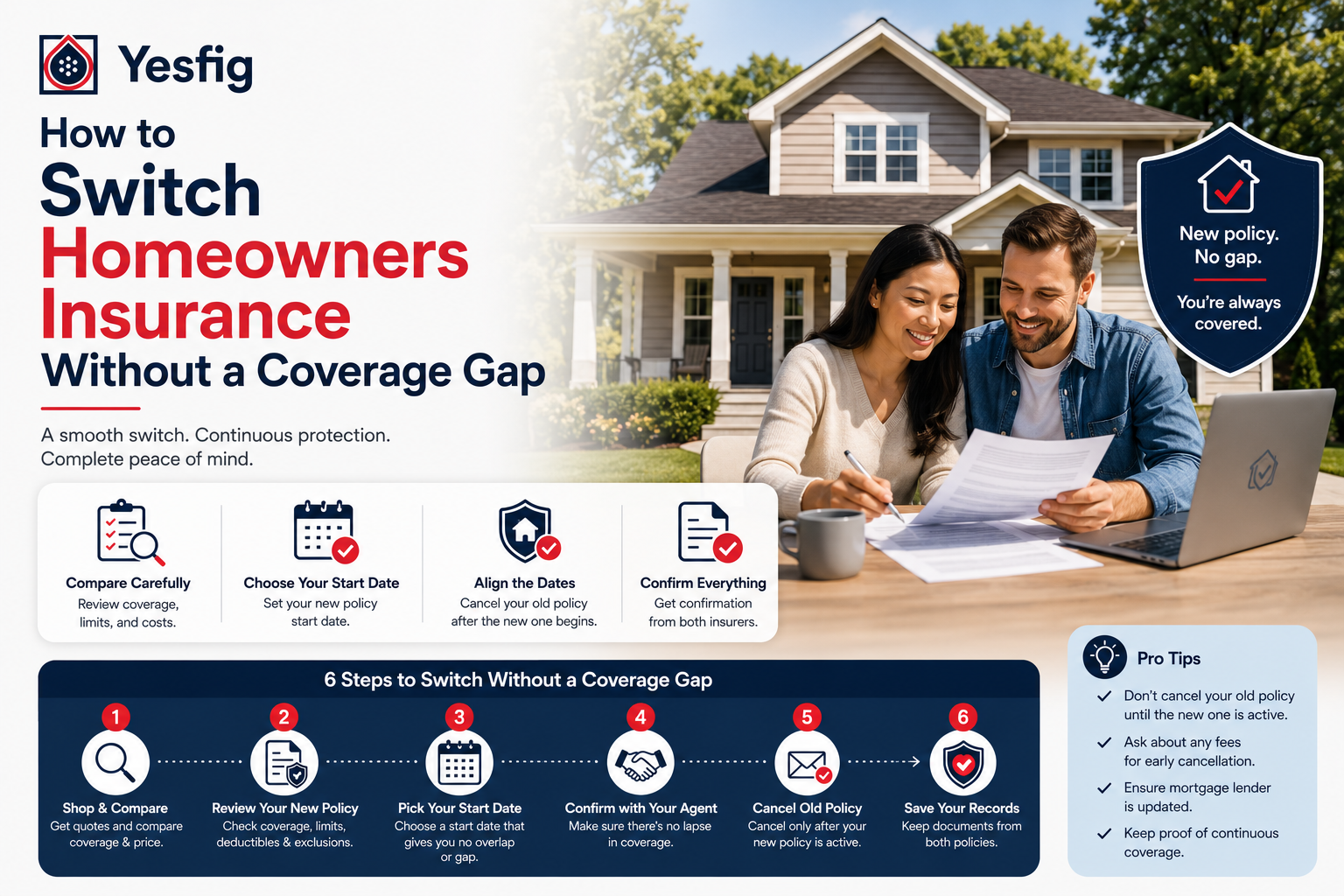

How to switch homeowners insurance without a gap

The whole switch comes down to three steps, in this order. Do them this way and a gap is almost impossible.

- Lock in the new policy first. Shop, compare, and get the new homeowners policy fully approved and bound before you touch your current one. Nothing gets canceled until the replacement is real.

- Match the dates. Set the new policy's effective date to the exact day your current policy ends. A one-day overlap is completely fine and costs you almost nothing. A one-day gap is the thing to avoid.

- Cancel the old policy after the new one is active, and tell your lender. Once the new coverage is live, cancel the old policy in writing and confirm the effective date. Then notify your mortgage lender so they update the policy on file and pay the right carrier.

That's it. The order is the whole trick: new policy on, then old policy off, with the dates touching.

Time the switch around your renewal and your mortgage

The cleanest moment to switch is your renewal date, because the old policy is ending anyway and there's a natural handoff. You're not canceling mid-term, you're just choosing not to renew and starting fresh with a new carrier the same day.

If your premiums are paid through an escrow account, loop in your lender early. They'll redirect payment to the new carrier, and you'll typically get a prorated refund of any unused premium from the old policy if you do switch mid-term. The same timing logic applies if you ever bundle your home and car insurance, since you'll want both effective dates to line up cleanly too.

Good to know: California's home insurance market has tightened because of wildfire risk, and some carriers have pulled back or stopped renewing in higher-risk areas. If you're switching, confirm the new carrier will write your specific property and ZIP before you cancel anything. The California FAIR Plan exists as a last-resort option, and the California Department of Insurance can help if you're struggling to find coverage.

Want to see how your current policy actually stacks up?

Yesfig reviews what you already have, maps where you're over- or under-covered, and shows you where the price or the protection could be better. Compare your homeowners coverage in a few minutes, no pressure to switch.

Mistakes that quietly leave you exposed

A few small missteps create the exact gap you're trying to dodge:

- Letting the old policy cancel for non-payment instead of formally replacing it. A lapse on your record can make the next policy cost more.

- Treating a quote or a binder as full coverage. A binder is temporary proof; make sure the actual policy is issued and active.

- Forgetting to update the lender, which can trigger that expensive force-placed insurance even when you do have a new policy.

- Downgrading coverage just to chase a lower price. Dropping from replacement cost to actual cash value saves a little now and can cost you a lot after a claim.

Key takeaways

- A coverage gap is any day your home has no active policy, and it puts both your house and your mortgage at risk.

- Always start the new policy before canceling the old one, with the dates touching.

- A one-day overlap is safe and cheap. A one-day gap is the expensive mistake.

- Switch at renewal when you can, and notify your mortgage lender so escrow pays the right carrier.

Frequently asked questions

Can I switch homeowners insurance at any time?

Yes. You can switch homeowners insurance whenever you want, not only at renewal. If you switch mid-term, you'll usually get a prorated refund of unused premium from your old carrier. Just make sure the new policy is active before you cancel the old one.

Will switching homeowners insurance hurt my mortgage?

No, switching is normal and lenders expect it. What matters to your lender is continuous coverage. As long as you keep the policy active and notify them of the new carrier and effective date, your mortgage and escrow account update without any problem.

Do I get money back if I cancel my old policy early?

Usually, yes. Most homeowners insurers issue a prorated refund for the unused portion of your premium when you cancel mid-term. If you paid through escrow, that refund typically flows back through your mortgage account, so confirm the details with both the carrier and your lender.

How long does it take to switch homeowners insurance?

A switch can often be set up in a day or two once you've chosen a new policy. The actual handoff happens on the effective date you pick. The smart move is to start shopping a few weeks before your renewal so the timing is relaxed, not rushed.

Is a one-day overlap between policies a problem?

No, a short overlap is harmless and is actually the safest way to switch. You might pay for one extra day of coverage, which is a few dollars at most. That tiny cost is worth avoiding any chance of an uninsured gap between your old and new policies.

Switch with confidence, not crossed fingers

Daniel made his switch the boring way: new policy bound, dates touching, old policy canceled the day after, lender notified. No gap, no drama, a lower premium, and a home that was covered every single day in between. That's the whole goal.

Yesfig Insurance, a brand of Focus Insurance Group based in Los Angeles, helps California homeowners do exactly that, with quotes in minutes and a licensed advisor on hand when you want one. You can always read more in the Yesfig insurance blog if you're still weighing your options.

Ready to make the switch?

Get a homeowners insurance quote with Yesfig, with coverage starting at $25/mo. Line up your start date, keep your home protected the whole way through, and let Fig handle the comparison while a real advisor stands by.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.