June 16, 2026

How to Switch Health Insurance Plans Without a Coverage Gap

How to switch health insurance plans without a coverage gap: time it right, align your effective dates, and avoid any days without coverage.

How to Switch Health Insurance Plans Without a Coverage Gap

Quick answer: To switch health insurance without a coverage gap, enroll in your new plan and confirm it's active before canceling the old one, and align the dates so your old coverage runs until the new plan begins. You can switch during open enrollment or after a qualifying life event, and a new plan usually resets your deductible.

Table of contents

- When you can switch health insurance plans

- How to switch health insurance without a coverage gap: it's all in the timing

- The step-by-step switch

- What to check before you switch

- The deductible reset trap

- How to switch health insurance smoothly in California

- Frequently asked questions

When Gabriel changed jobs in Sacramento, he assumed his health coverage would simply hand off from the old plan to the new one. It doesn't work that way. His new plan wouldn't start for several weeks, and canceling the old one too early would have left him uninsured in between. Knowing how to switch health insurance plans without a coverage gap is the difference between a clean transition and a stressful month hoping nobody gets sick.

A gap of even a few days can mean paying full price for care or a prescription. The good news is that avoiding one comes down to timing, and timing is something you can plan.

When you can switch health insurance plans

You can't always change plans on a whim, so the first step is knowing your window. There are two main openings.

Open enrollment is the annual period when anyone can enroll in or change a plan, generally in the fall and early winter. It's the simplest time to switch, with no special reason required.

A special enrollment period opens after a qualifying life event, such as losing other coverage, getting married, having a baby, or moving. These typically give you a limited window, often around 60 days, to make a change outside of open enrollment.

If you're switching because of a new job or other life change, you're usually in special-enrollment territory. Knowing which applies tells you what's possible and when, and a new health insurance plan starts with that clarity.

Worried about a gap between plans?

That's the right thing to watch for. Fig can walk you through the timing so your old and new coverage line up cleanly, in plain English. Start with the basics of health insurance in California.

How to switch health insurance without a coverage gap: it's all in the timing

A gap happens for one reason: the old plan ends before the new one begins. Avoid that overlap problem and you avoid the gap entirely.

Most plans take effect on the first of a month, and when you enroll can determine whether coverage starts next month or the month after. That detail is exactly where people slip up, canceling old coverage on an assumption about when the new plan kicks in.

Good to know: Never cancel your old health plan until the new one is confirmed active, or you risk days without coverage. Switching to a new plan usually resets your deductible and out-of-pocket maximum to zero. In California, Covered California's open enrollment window is typically longer than the federal one. Yesfig offers health coverage in California and five other states.

The safe rule is simple: keep the old coverage running until the new plan's start date has arrived and you've confirmed it's active. A brief overlap costs little; a gap can cost a lot.

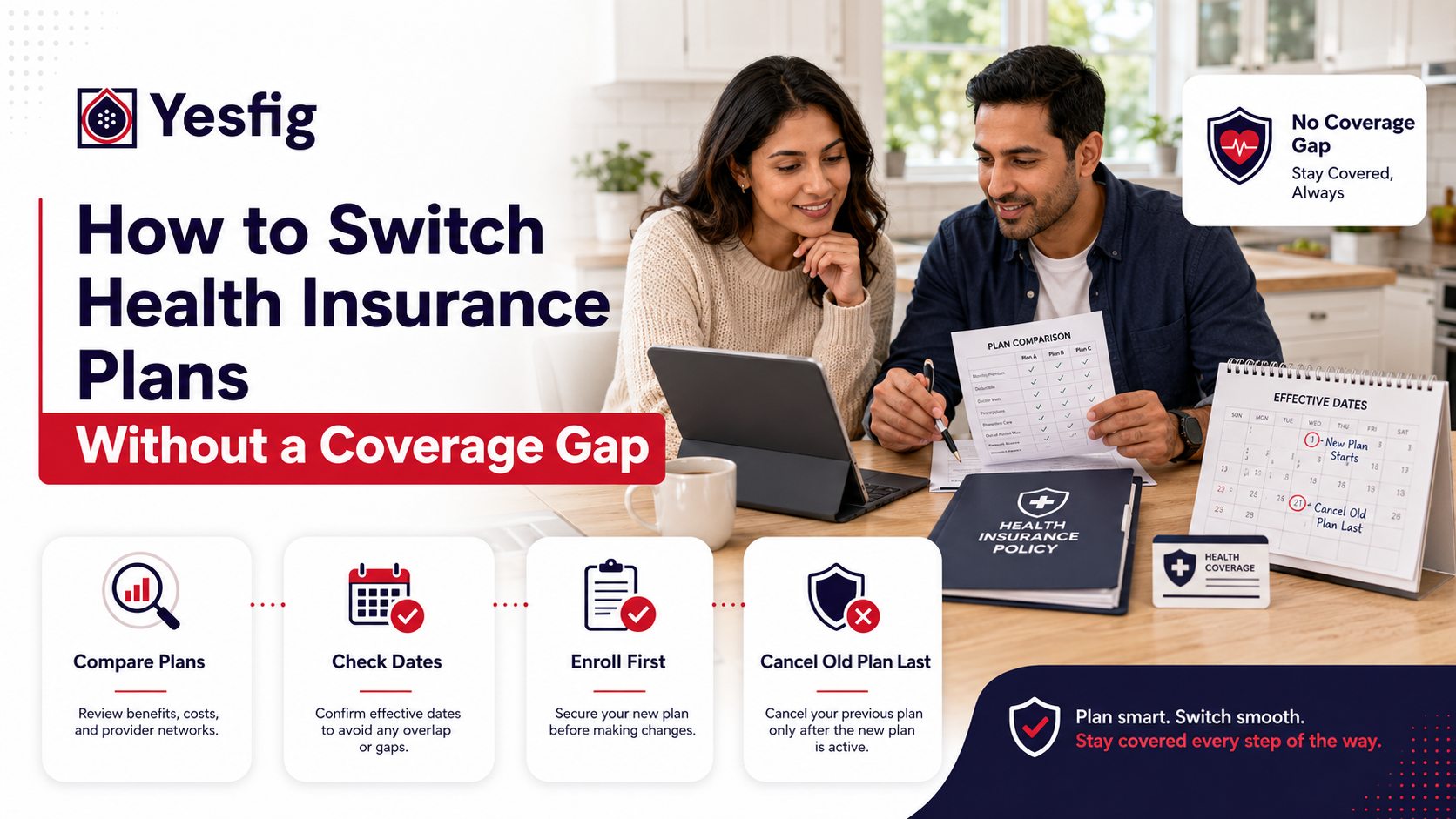

The step-by-step switch

Here's the clean sequence Gabriel followed to switch without a single uncovered day.

- Confirm your eligibility. Verify you're in open enrollment or have a qualifying life event that opens a special enrollment period.

- Choose the new plan and note its start date. Know exactly when coverage will begin before you do anything else.

- Enroll and confirm it's active. Complete enrollment and wait for confirmation, like a member ID, that the new plan is in force.

- Then end the old plan. Set the old coverage to end on or after the new plan's start date, so the two meet or briefly overlap.

- Transfer your care. Move prescriptions to the new plan and confirm your providers before the switch takes effect.

The order matters most at steps three and four. New plan active first, old plan canceled second, never the reverse.

Key takeaways

- You can switch during open enrollment or after a qualifying life event.

- Confirm the new plan is active before canceling the old one.

- Align effective dates so coverage overlaps, never leaving a gap.

- A new plan usually resets your deductible, so time it thoughtfully.

What to check before you switch

A gap-free switch to the wrong plan is still a problem. Before you commit, check three things on the new plan:

Your doctors. Confirm your current providers are in-network, since an out-of-network switch can mean higher costs or starting over with new doctors.

Your prescriptions. Check the plan's formulary to make sure your medications are covered, and at what tier, so nothing gets expensive overnight.

Your real costs. Compare the premium, deductible, and out-of-pocket maximum together, not just the monthly price, so the new plan actually fits how you use care.

Catching these before the switch beats discovering them at the pharmacy or doctor's office afterward.

The deductible reset trap

This is the part people forget, and it can sting if you switch mid-year. When you move to a new plan, your deductible and out-of-pocket maximum usually reset to zero. The amounts you already paid this year generally don't carry over.

So if you've already met most of your deductible and then switch plans in, say, August, you could be starting that spending from scratch on the new plan. It doesn't mean you shouldn't switch, but it's a real cost to weigh in the timing.

When the switch is your choice rather than forced by a life event, lining it up with the start of a plan year often avoids this reset. If you're switching from a group health plan to an individual one or vice versa, the same reset usually applies.

How to switch health insurance smoothly in California

California gives you a little more runway. Covered California, the state marketplace, typically runs a longer open enrollment window than the federal one, which gives you extra time to plan a clean switch.

Special enrollment periods still apply for qualifying life events like a job change, marriage, or move, usually with a limited window to act. The same timing rules hold: enroll, confirm the new plan is active, then end the old one. Yesfig Insurance, a brand of Focus Insurance Group based in Los Angeles, can help you line up the dates so your California switch has no gap.

Not sure which new plan to switch to?

The switch is only as good as the plan you land on. Yesfig can help you compare networks, prescriptions, and costs so your new plan actually fits. Compare health plan options before you switch, or ask a licensed Yesfig advisor to check the timing.

Frequently asked questions

Can I switch health insurance plans anytime?

Not usually. You can change plans during the annual open enrollment period, or after a qualifying life event like losing coverage, marriage, a birth, or a move, which opens a special enrollment period of limited length. Outside those windows, switching generally isn't allowed, so knowing which applies to you is the first step.

How do I avoid a gap when switching health insurance?

Keep your old plan active until the new one has started. Enroll in the new plan, confirm it's in force, and only then set the old coverage to end on or after the new start date. Because plans often begin on the first of a month, aligning those dates carefully is what prevents any uncovered days.

Does my deductible reset when I switch health plans?

Usually, yes. Moving to a new plan typically resets your deductible and out-of-pocket maximum to zero, and amounts you already paid this year generally don't transfer. If you switch mid-year after meeting much of your deductible, you may start over. When the timing is your choice, switching at the start of a plan year often avoids this.

What is a qualifying life event for health insurance?

A qualifying life event is a change that opens a special enrollment period outside open enrollment. Common examples include losing existing coverage, getting married or divorced, having or adopting a child, and moving to a new area. These events usually give you a limited window, often around 60 days, to enroll in or switch plans.

Should I cancel my old plan before the new one starts?

No. Canceling the old plan before the new one is active is the most common way people end up with a coverage gap. Always confirm the new plan has started, ideally with a member ID or written confirmation, before ending the old coverage. A short overlap is far safer than even a few uncovered days.

A clean switch is a planned one

Switching health insurance without a gap isn't complicated, but the order is everything: enroll, confirm, then cancel, with the dates lined up so coverage never lapses. Check your doctors and prescriptions on the new plan, mind the deductible reset, and you're set. Like Gabriel did, you can change plans and never spend a single day uninsured.

Ready to switch without the stress?

Explore health insurance with Yesfig and a licensed advisor can help you time the change so there's no gap and no surprise. Getting the dates right is the whole game.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.