June 16, 2026

Homeowners Insurance for Older Homes: What You Need to Know

Homeowners insurance for older homes costs more and asks harder questions. Here's what affects your rate and the coverage an older house really needs.

Homeowners Insurance for Older Homes: What You Need to Know

Quick answer: Homeowners insurance for older homes often costs more because aging wiring, plumbing, and roofs raise the risk of claims, and unique materials cost more to rebuild. Insurers may ask about your systems or require updates. Adding ordinance-or-law and replacement-cost coverage, and documenting any upgrades, helps you get solid coverage at a fair price.

Table of contents

- Why older homes are harder to insure

- What insurers look at in an older home

- The coverage older homes especially need

- What homeowners insurance for older homes costs more for

- How to get and keep affordable homeowners insurance for older homes

- What California adds for older homes

- Frequently asked questions

When Priscilla bought a 1920s Craftsman in Pasadena, she fell for the original woodwork and the wraparound porch. Her insurance quote fell a little harder. The same features that gave the house its character, its age, its wiring, its hand-built details, also made it trickier to insure. If you own or are eyeing an older property, homeowners insurance for older homes comes with a few wrinkles worth understanding before you sign anything.

None of them are dealbreakers. They're just things to know going in, so the quote doesn't catch you off guard and the coverage actually fits the house. Here's the full picture.

Why older homes are harder to insure

It comes down to two things: risk and rebuild cost. Older homes tend to have aging systems that fail more often, which means more potential claims, and insurers price that in.

The second factor is subtler. An older home may be built with materials and craftsmanship that are expensive or hard to replicate today, like plaster walls, custom millwork, or specific framing. If it's damaged, rebuilding to match can cost more than a comparable modern home, which raises the coverage you need.

So a charming old house isn't being penalized for its charm. It's being priced for the real cost of insuring and rebuilding it. The good news is that much of that cost is manageable once you know the levers, starting with a tailored quote on a homeowners policy.

Quoted more than you expected on an older home?

That's common, and often fixable. Fig can explain why an older house prices the way it does and where you can bring it down, in plain English. Start with the basics of homeowners insurance in California.

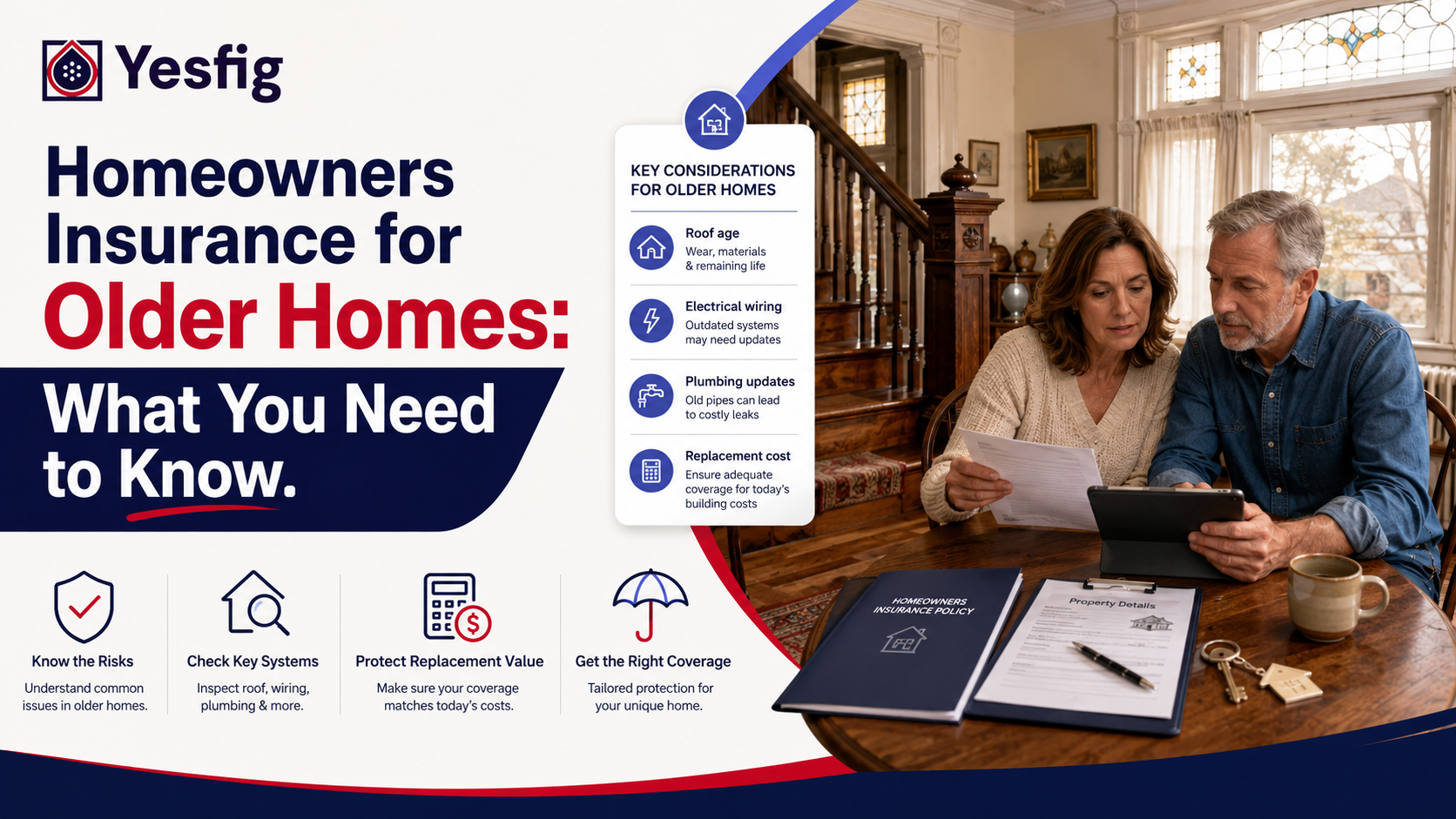

What insurers look at in an older home

When you insure an older property, expect questions about its systems. These four are where most of the attention goes:

- Electrical. Older wiring like knob-and-tube or aluminum, and fuse boxes instead of breaker panels, are common concerns. Some insurers want them updated.

- Plumbing. Galvanized steel or polybutylene pipes are prone to failure and corrosion, which insurers watch closely.

- Roof. Roof age matters a lot. An older roof may only be covered at depreciated value, or may need replacement to qualify for full coverage.

- Heating and HVAC. Outdated systems and certain older heat sources can raise risk and affect your rate.

You may be asked for an inspection or documentation on these. Knowing what they're checking lets you get ahead of it rather than be surprised by it.

The coverage older homes especially need

A standard policy isn't always enough for an older house. A few coverages matter much more here than they do for new construction.

Ordinance or law coverage is the big one. When you repair or rebuild an older home, current building codes apply, and bringing an old structure up to code can be expensive. This coverage pays that added cost, and older homes often need more of it than a basic policy includes.

Replacement cost versus actual cash value is the other. With actual cash value, payouts are reduced for depreciation, which hits older homes hard. Replacement cost coverage pays to rebuild at current prices, which is usually the safer choice for an older property.

Good to know: Older homes especially need ordinance-or-law coverage, which pays the added cost of meeting current building codes when you rebuild or repair. In California, standard policies still exclude earthquake and flood, and retrofitting an older home can reduce earthquake risk. Yesfig offers homeowners coverage in California and five other states.

Getting these two right is often the difference between a policy that rebuilds your home and one that leaves a gap.

Key takeaways

- Older homes cost more to insure because of aging systems and pricier rebuilds.

- Insurers care most about wiring, plumbing, roof, and heating.

- Ordinance-or-law coverage is especially important for older homes.

- Documenting updates and comparing insurers keeps the price fair.

What homeowners insurance for older homes costs more for

The premium reflects specific risks, and naming them shows you where to focus. Older homes typically cost more to insure because of:

- Outdated electrical and plumbing that raise the odds of fire or water damage claims.

- An aging roof that's closer to needing replacement.

- Higher rebuild costs from unique or period-specific materials.

- Code-upgrade expense, since rebuilding triggers current building standards.

Each of these is also a clue about what to improve. Address the systems that drive the cost, and you address the premium at the same time.

How to get and keep affordable homeowners insurance for older homes

You have more control than the first quote suggests. Work these steps to land solid coverage at a fair price:

- Document your updates. Keep records of any work on wiring, plumbing, the roof, and HVAC, since updated systems can lower your rate or unlock coverage.

- Prioritize the upgrades insurers value. A panel upgrade, repiping, or a newer roof often moves the premium the most.

- Add the right coverage. Make sure ordinance-or-law and replacement-cost protection match your home's age and rebuild cost.

- Compare insurers. Appetite for older homes varies widely, so shopping around can mean very different rates for the same house.

Done together, these turn an intimidating quote into a manageable one. A licensed Yesfig advisor can help you figure out which upgrades and coverages matter most for your specific home, and bundling with an auto policy can trim the overall bill.

What California adds for older homes

California owners of older homes have two extra things to weigh. First, standard policies exclude earthquake and flood, and older homes can be more vulnerable to seismic damage, so earthquake coverage and retrofitting are worth considering. Strengthening an older home's foundation can reduce both risk and worry.

Second, wildfire risk affects availability and pricing in many areas, and the California FAIR Plan exists as a backstop if standard coverage is hard to find. Factoring these in early helps you build a complete picture rather than discovering a gap later. Yesfig Insurance, a brand of Focus Insurance Group based in Los Angeles, can help you sort what an older California home needs.

Not sure your older home is covered the right way?

Older houses need specific coverage that standard quotes can miss. Yesfig can check that your policy includes the right ordinance-or-law and replacement-cost protection for your home's age. Review homeowners coverage built for an older house.

Frequently asked questions

Why is homeowners insurance more expensive for older homes?

Older homes tend to have aging electrical, plumbing, and roofing that raise the risk of claims, and they often use materials that cost more to rebuild. Insurers price both factors in. Code-upgrade expenses when rebuilding add to the cost too. Updating key systems and documenting that work can help bring the premium down.

What home systems do insurers care about most in an older house?

Electrical, plumbing, roof, and heating top the list. Insurers watch for older wiring like knob-and-tube or aluminum, fuse boxes, galvanized or polybutylene pipes, an aging roof, and outdated heating systems. These affect the odds of fire and water damage claims, so updates to any of them can improve both your coverage options and your rate.

What is ordinance or law coverage and why do older homes need it?

Ordinance or law coverage pays the extra cost of meeting current building codes when you repair or rebuild. Older homes often weren't built to today's standards, so bringing them up to code after a loss can be expensive. A basic policy may include only limited amounts, so older homes frequently need more of this coverage.

Can updating an old home lower my insurance cost?

Often, yes. Upgrading the systems insurers worry about most, like the electrical panel, plumbing, or roof, can reduce your premium and sometimes make coverage available that wasn't before. Keeping documentation of the work matters, since insurers want proof. Even partial updates to high-risk systems can improve both your rate and your options.

What's the difference between replacement cost and actual cash value for an old home?

Replacement cost pays to rebuild at today's prices with no deduction for age, while actual cash value subtracts depreciation, which can sharply reduce payouts on an older home. For older properties, replacement cost coverage is usually the safer choice, since actual cash value can leave a large gap between the payout and the real rebuild cost.

An older home is worth insuring well

The features that make an older home special are the same ones that make its coverage a little more involved. Understand the systems insurers care about, add ordinance-or-law and replacement-cost protection, document your upgrades, and compare carriers. Like Priscilla did with her Craftsman, you can protect a home with history without paying more than you should.

Ready to insure your older home properly?

Get a homeowners insurance quote with Yesfig and a licensed advisor can match your coverage to your home's age, systems, and rebuild cost, so nothing important is missing.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.