June 3, 2026

HMO vs PPO vs EPO Health Plans: Which One Fits You?

HMO vs PPO vs EPO: compare costs, doctor networks, and referral rules to pick the California health plan that actually fits your life and budget.

HMO vs PPO vs EPO: How to Pick the Health Plan That Fits You

Quick answer: HMO vs PPO vs EPO comes down to flexibility versus cost. HMOs are cheapest but need referrals and in-network care. PPOs cost more and let you see almost anyone, even out-of-network. EPOs sit in the middle: lower premiums, no referrals, but in-network only. Your doctors and budget decide.

Table of contents

- What HMO, PPO, and EPO actually mean

- HMO vs PPO vs EPO: the quick comparison

- When an HMO is the right call

- When a PPO is worth paying more for

- Where an EPO fits in

- HMO vs PPO vs EPO: how to pick what fits you

- Frequently asked questions

- Picking a plan you won't second-guess

Daniel, a freelance designer in Sacramento, opened his enrollment options and found three letters staring back: HMO, PPO, EPO. Same insurer, similar-looking prices, completely different rules. He's not alone in the low-grade panic that follows.

Here's the thing: the HMO vs PPO vs EPO question isn't really about the acronyms. It's about how much you'll pay, which doctors you can keep, and how many hoops you'll jump through to get care. Sort those three out and the right plan tends to pick itself.

What HMO, PPO, and EPO actually mean

These are plan types, not insurers. They describe how a health plan handles your doctor network and whether you need a referral to see a specialist.

An HMO (Health Maintenance Organization) keeps care inside a set network and asks you to pick a primary care physician (the doctor who coordinates your care and writes referrals). A PPO (Preferred Provider Organization) skips the referral step and pays a share even when you go out-of-network. An EPO (Exclusive Provider Organization) is the hybrid: no referrals like a PPO, but in-network only like an HMO.

Premiums usually rise as flexibility rises. That's the trade you're weighing across all three California health insurance options, and it's the same logic whether you're shopping solo or comparing a workplace plan.

Still sorting out the basics?

That's exactly what Fig is for. Get plain-English answers on how each plan type works, then walk through the Yesfig insurance blog for more before you commit to anything.

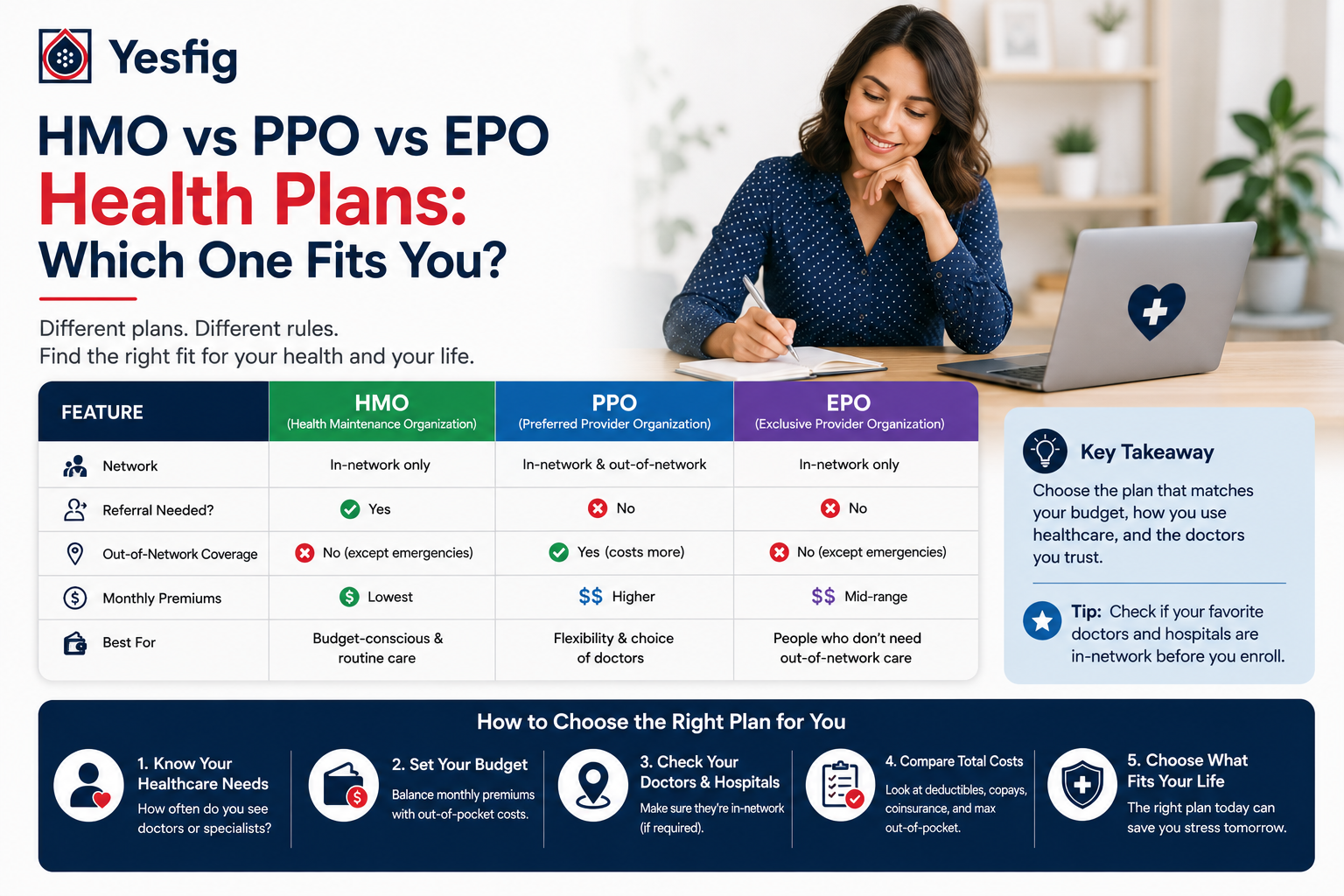

HMO vs PPO vs EPO: the quick comparison

Side by side, the differences get a lot clearer:

| Feature | HMO | PPO | EPO |

|---|---|---|---|

| Monthly premium | Lowest | Highest | Moderate |

| Need a referral for specialists? | Yes | No | Usually no |

| Out-of-network coverage? | No (emergencies only) | Yes, at a higher cost | No (emergencies only) |

| Primary care physician required? | Usually | No | Sometimes |

| Best for | Cost-conscious, in-network care | Flexibility and frequent specialists | A middle path |

No single column wins. A plan that's perfect for a healthy 26-year-old can be a poor fit for a parent managing a chronic condition across several specialists.

Key takeaways

- HMOs trade flexibility for the lowest premiums and tight networks.

- PPOs cost the most but give you the widest choice of doctors.

- EPOs land in between: no referrals, but you stay in-network.

- The right pick depends on your doctors and your budget, not on which type sounds best.

When an HMO is the right call

An HMO makes sense when you want the lowest monthly cost and don't mind staying inside a network. If you're generally healthy, see one doctor a year, and live somewhere with strong in-network coverage, the savings are real.

The catch is the referral system. Want to see a dermatologist? You go through your primary care physician first. For some people that feels like a gatekeeper; for others it's a helpful traffic cop who keeps care coordinated. In California, many HMOs are regulated by the Department of Managed Health Care, which sets timely-access standards for appointments.

The risk is going out-of-network. Outside emergencies, an HMO generally won't pay, so if your preferred specialist isn't in the network, that visit is on you.

When a PPO is worth paying more for

A PPO earns its higher premium when flexibility actually matters to your life. No referrals, a broad network, and partial coverage even when you step out-of-network, all of which buys you room to choose.

Picture someone who travels for work, splits time between Los Angeles and the Bay Area, or sees several specialists who don't share one network. A PPO lets them keep those relationships without asking permission first. That freedom is the whole point.

Just know what you're paying for. PPOs typically carry higher deductibles and out-of-pocket costs alongside the bigger premium. If you rarely leave your network anyway, you may be paying for flexibility you won't use.

Want to see how your options stack up?

Yesfig reviews what each plan really costs you, maps the network gaps, and shows where you can improve price or coverage. Compare California health plans in a few minutes, no pressure to switch.

Where an EPO fits in

An EPO is for people who want PPO-style freedom without the PPO price. You skip the referral dance and usually don't need a primary care physician, but you stay in-network like an HMO. For a lot of healthy folks, that's the sweet spot.

The trade is the same one HMOs make: go out-of-network for anything but an emergency and you're paying full freight. So an EPO works best when the network is large and already includes the doctors you care about.

Self-employed Californians often land here. If you're shopping the individual market or a small-team plan, it's worth comparing EPOs against group health plans to see which structure fits your situation and your headcount.

HMO vs PPO vs EPO: how to pick what fits you

Forget which type sounds best on paper. Work the decision backward from your actual care:

- List your must-keep doctors and any specialists you see regularly.

- Match that list against each plan's network and referral rules. A plan that drops your cardiologist is a non-starter, no matter the premium.

- Get a quote, compare the true monthly cost, and lock in the plan that covers your people.

That order keeps you from overpaying for flexibility you don't need, or underpaying into a network that doesn't have your doctor.

Good to know: In California, most individual and family plans are sold through Covered California, the state marketplace, where you can also check if you qualify for premium subsidies. Comparing the same plan type across carriers there can change the math more than switching types.

Yesfig Insurance, a brand of Focus Insurance Group based in Los Angeles, helps with exactly this comparison: it reviews your current coverage, flags the gaps, and lays the plans side by side so the choice is obvious. You can learn more about how Yesfig works and lean on a licensed advisor whenever you want a human in the loop.

Frequently asked questions

Is an HMO or PPO better if I'm healthy?

For a healthy person who rarely sees specialists, an HMO or EPO usually wins on cost, since you give up flexibility you wouldn't use anyway. A PPO mainly pays off when you see multiple specialists, travel often, or want out-of-network freedom worth the higher premium.

Can I see a specialist without a referral on an EPO?

Usually yes. EPOs typically let you book a specialist directly without a referral, which is one of their biggest advantages over an HMO. The catch is that the specialist must be in-network, because EPOs only cover out-of-network care in a true emergency.

What happens if I go out-of-network on an HMO or EPO?

Outside of emergencies, an HMO or EPO generally pays nothing for out-of-network care, leaving the full bill to you. PPOs are the exception: they still cover a share of out-of-network costs, though at a higher rate than you'd pay in-network.

What's a POS plan, and how is it different?

A POS (Point of Service) plan blends HMO and PPO features. Like an HMO, it asks for a primary care physician and referrals. Like a PPO, it covers some out-of-network care. It's less common than the three main types but worth a look if you want a middle ground.

Does Yesfig offer health plans outside California?

Yes. While Yesfig is California-first, its health coverage is also available in Texas, Illinois, Pennsylvania, Ohio, and Florida. Term life and accidental death, by contrast, are California-only. For health plans, you can compare options in any of those six states.

Picking a plan you won't second-guess

By the time Daniel mapped his two doctors against each network, the HMO vs PPO vs EPO choice basically made itself. Both were in the EPO network, so he got PPO-style freedom at a lower price and stopped overthinking it.

That's the goal: a plan that fits your doctors, your budget, and your life, chosen once and not fretted over again. Real coverage, handled, so you can get back to everything else.

Ready to find your fit?

Get a California health insurance quote with Yesfig in minutes. Plans start at $50/mo, and a licensed advisor is on hand the moment you want one.

About the Author

Mathew Bahadori

CEO, Yesfig Insurance

Leading the company’s mission to make insurance more accessible, modern, and customer-focused. With a passion for innovation and personalized service, he continues to help individuals and families find smarter coverage solutions for life, auto, home, health, and business insurance.